To use (and abuse) my good friend Sangeet Paul Choudary‘s framework, Twitter is both a pipe and a platform. Whether it is a pipe or a platform depends on how you use it.

I always use Twitter in the “latest tweets” mode, which means that tweets from people I follow are shown to me in the order in which they happen, with most recent tweets on top. Twitter has no role in showing what tweets I see or not see. Someone I follow says something, it will come in its appointed place. This is the twitter in its “pipe avatar”. It is no different from reading blogs through an RSS feed. Twitter is just a pipe to convey these tweets to me.

However, this “latest tweets” is not the default mode for Twitter. The default mode is what I think it calls “top tweets” or something. This is the algorithmic timeline that Twitter launched a few years back. Here, twitter’s algorithms determine what you should see. Whether a tweet gets shown to you at all, whether you follow someone whose tweets you are shown and what order tweets are shown to you in – none of these are under your control. It is twitter’s (rather, and understandably, opaque) algorithm that determines this. This is twitter operating in its “platform avatar”, since it, through its algorithms, is effectively controlling the content you see.

Why is it important if twitter is a pipe or a platform? It has to do with regulation. I understand that twitter and facebook have recently suspended Donald Trump’s account. Some people are saying this is unfair, and that it is a step too far for social media. Others are using this as an excuse for more social media regulation.

My contention is that whether social media should be regulated or not is guided by whether social media is a pipe or a platform.

If social media is a pipe, like twitter in its latest tweets (or “traditional”) format, then regulation is unnecessary. In this situation, people are served tweets only because they’ve chosen to receive them. If some account only tells lies, so be it. People follow parody accounts all the time. By censoring accounts, twitter is denying people the right to see the thing they have subscribed to see. Any regulation or censorship means that people are not getting what they have signed up for.

On the other hand, in the algorithmic timeline format, one can make a case for some kind of regulation or censorship. This is because the platform here, either implicitly or explicitly, chooses what the user sees. And if the platform’s algorithms mean that lies and hatred and outrage get amplified, then that is a problem. If a tweet from a parody account suddenly appears in my timeline, it can throw me off and drive me bonkers. And that is not “fair”.

Then again, while one can make a case for censorship in the “platform model”, I’m not advocating that regulation or censorship is necessary. Yes, the opaque algorithms can amplify bad shit, but how are you going to even regulate that?

You want algorithms to be passed by some central board? You want the platform to deplatform your opponents but not your folks? You want a profit-maximising (likely monopoly) private entity to determine what is “truth” and what is not? Irrespective of how the regulation or censorship is defined, it is rather easy for it to have consequences that the designers of the regulation or censorship have least expected.

In any case, these occasional cals for censorship or regulation or cancellation are the reasons why I put most of my better arguments on this blog, which gets delivered through this pipe called RSS feeds.

Being married to Marriage Broker Auntie means that I sometimes get to participate, either directly or indirectly, in some of her “experiments”. Her latest experiment was to get on to dating apps, to see what the hell they are all about, so that she can advise her clients better about them.

She has written about her experience on these apps in the latest edition of her newsletter. Oh, and you should totally subscribe to her newsletter if you haven’t already. You will get some very interesting relationship insights, which you can appreciate even if you aren’t looking for a relationship.

Anyways, once she started her latest experiment, I asked myself “why should girls have all the fun?”, and got curious to get on these apps myself. I spoke to her about it, and she suggested that I check out Hinge. “It’s the most decent among all the apps”, she said.

I mean, this wasn’t my first time on a dating app. Though they all appeared well after I had got married, I remember trying out Tinder a few years back, possibly as part of another of my wife’s experiments. I remember getting disillusioned by it and deleting it in less than a day. I had even forgotten about it, except that when I was searching for Hinge on the app store, I found that I had already “bought” Tinder in the past (I now realise I’d tried TrulyMadly in the past as well – yet another unmemorable experience).

Anyways, I quite liked Hinge. I spent a whole week on it, before I decided that people who don’t know what’s happening might think I’m a creep and deleted my account.

What makes Hinge so nice is the way it is structured and the user experience. For starters, there’s no easy swiping left or right – there are (fairly small) buttons to either like or dismiss a profile, and in case there has been a mutual like, then there is a “match” and you can start chatting.

Also, from one little experiment (where the wife and I decided to like each other on Hinge), I found that Hinge has implemented something that I have always believed in – basically don’t tell both parties that there is a match immediately after the second person has liked. That way, the pair know who liked whom first and that can set an unhealthy prior in the relationship. Instead, if the app waits for a “random period of time” before announcing the match, you don’t know who liked whom first.

Back to Hinge – what I liked about it was how the profiles had been designed. You are asked to upload six photos of yourself doing different things, and also answer a few questions. The answers to these questions are displayed in bold on your profile, and this means that anyone who pays some amount of attention is likely to see these answers.

This means that you don’t need to impress your potential counterparties with your photos (or one photo) alone – you can show off your “well rounded personality” (if you have one that is). For example, I found this girl whose profile seemed unremarkable until I saw that she “got turned on by probability and maths”. That, of course, grabbed my attention and I immediately paid much more attention to her full profile. This kind of information (conveying your possibly unusual interests) is a little hard to get across on other dating platforms.

The other nice thing about Hinge is that you can choose what part of a person’s profile you want to like. You could choose one of the pictures, for example, or one of their answers to some question. Like if I were actually in the market (and not casually “researching”) I would have tried to start a conversation with the above mentioned person by liking (and possibly commenting on) her interest in probability.

This specific liking provides an automatic conversation starter. And in a congested market (see chapter 4 of my book here), anything that can help you distinguish yourself can be a sure winner. So it helps that you can write about your interest in probability. It helps that you can tell someone you like her for her interest in probability and not for her tattoo. In marketing jargon, it allows you to be “a qualified lead”.

I had fun for about a week. I must mention that I had used my real name (rather, my oldest nickname that everyone knows me by), and my real photo (my wife picked that one) on the platform. And then I got likes from two women (apart from the one from my wife).

Given that I’m not actually looking for a relationship, that made me feel like I’m doing something wrong. I felt horrible about myself for putting myself on a dating app when I’m not looking to date. There was also the thing that people who found me on the app and knew me would think of me as a creep (or get the wrong kind of ideas about my marriage). So I deleted it.

However, if you are in the market and looking to date, I strongly recommend Hinge. Among the apps that I’ve used, it’s easily among the best.

Every time we have a sort of financial crisis that has something to do with settlement, and collaterals, and weird instruments, people start questioning why more instruments are not traded on exchanges. They cite the example of equities, which world over are exchange traded, centrally settled, and whose markets function rather efficiently.

After the 2008 Financial Crisis, for example, there was a move to take Credit Default Swaps (CDS) to exchanges, rather than letting the market go over the counter (OTC). Every few years, ideas are floated about trading bonds on exchanges (rather than OTC, like they are now), and the blame falls on “greedy bankers who don’t want to let go of control”.

There is an excellent podcast by Bloomberg Odd Lots where Chris White, a former Goldman Sachs banker, talks about how the equity markets went electronic in the 1970s with NASDAQ, and how the “big bang” in the UK markets propelled equities into electronic trading everywhere.

In any case, I think I have the perfect explanation of why bond trading on exchanges hasn’t really taken off. To understand this, let’s look at another market that I discussed extensively in my book – the market for relationships (that chapter has been extracted in Mint).

The market for relationships is in the news thanks to this Netflix documentary called Indian Matchmaking. I started watching it on a whim on Saturday night, and I got so addicted to it that yesterday I postponed my work to late night so that I could finish the show instead.

Marriage can be thought of as a sale of “50% of the rest of your life“, paid for by 50% of the rest of someone else’s life.

There are two ways you can go about it – either “over the counter” (finding a partner by yourself) or “exchange traded” (said exchange could be anything from newspaper classifieds to Tinder to Shaadi.com). Brokers are frequently used in the OTC market – either parents or friends (who set you up) or priests.

The general rule of markets is that the more bespoke (or “weird” or “unusual”) an instrument is, the better the likelihood of finding a match in the OTC markets than on exchanges. The reason is simple – for an exchange to exist, the commodity being traded needs to be a commodity.

Read any literature on agricultural markets, for example, and they all talk about “assaying” and “grading” the commodities. The basic idea is that all goods being traded on a marketplace are close enough substitutes of each other that they can be interchanged for each other.

Equity shares, by definition, are commodities. Equity and index derivatives are commodities as well, easy enough to define. Commodities are, by definition, commodities. Bond futures are commodities, since they can be standardised on a small number of axes. We’ll come to bonds in a bit.

Coming back to relationship markets, the “exchanges” work best if you have very few idiosyncrasies, and can be defined fairly well in terms of a small number of variables. It also helps you to find a partner quicker in case many others in the market have similar attributes as you, which means that the market for “your type of people” becomes “liquid” (this is a recurring theme in my book).

However, in case you are either not easily describable by commonly used variables, or in case there are few others like you in the market, exchanges are likely to work less well for you. Either of these conditions makes you “illiquid”, and it is not a great idea to list an illiquid asset on an exchange.

When you list an illiquid asset on an exchange, unless you are extremely lucky, it is likely to sit there for a long time without being traded (think about “bespoke exchanges” like eBay here, where commodification is not necessary). The longer the asset sits on an exchange, the greater the likelihood that people who come across the asset on the exchange think that “something is wrong with it”.

So if you’re listing it on an exchange, its value will decay exponentially, and unless you are able to trade soon after you have listed it, you are unlikely to get much value for it.

In that sense, if you are “illiquid” for whatever reason (can’t be easily described, or belong to a type that few others in the market belong to), exchanges are not for you. And if you think about each of the characters in Indian Matchmaking who come to Sima aunty, they are illiquid in one way or another.

Aparna has entered the market at 34, and few other women of her age are in the market. Hence illiquid.

Nadia belongs to a small ethnicity, Indian-Guyanese-American, which makes her illiquid.

Pradhyuman has quirky interests (jewelry and fashion), which his parents are trying to suppress as they pass him off a liquid “rich Maadu boy”. Quirky interests mean he’s not easily describable. Hence illiquid.

Vyasar, by Indian-American standards, doesn’t have a great job. So not too many others like him. Illiquid, even before you take his family situation into account.

Ankita is professionally ambitious. Few of those women in the Indian arranged marriage market. Illiquid.

Rupam is divorced with a child. Might be liquid by conventional American markets, but illiquid in an Indian context. And she is, rather inexplicably, going the Indian way despite being American.

Akshay is possibly the most liquid (characterless except for an overly-dominating mom), and maybe that’s why he’s shown getting engaged.

All of these people will be wasting themselves listing themselves on exchanges. And so they come to a matchmaker. Now, Sima Auntie is both a broker and a clearinghouse (refer to Chapter 3 of my book 😛). She helps find matches for people, but only matches within her own inventory (though she decided Ankita has no matches at all in her own inventory, so connected her with another broker-clearinghouse).

This makes it hard – first of all you have illiquid assets, and you are trying to fulfil them within limited inventory. This is why she is repeatedly showing saying that her candidates need to “compromise” (something that seems to have triggered a lot of viewers). By compromise, she is saying that these people are so illiquid that in case they need to get a deal in her little exchange, they need to be willing to accept an “illiquidity discount” in order to get a trade.

Back to bonds, why is trading them on an exchange so difficult? Because each bond is so idiosyncratic. There is the issuer, the exact date of expiry and the coupon, and occasionally some weird derivatives tacked on. The likelihood that you might find someone quickly enough to take the other side of such a deal is minuscule, so if you were to list your bond on an exchange, its value would drop significantly (by being continuously listed) before you could find a counterparty.

Hence, people trade this uncertain discount to a certain discount, by trading their bonds with market makers (investment banks) who are willing to take the other side of the deal immediately.

Unfortunately, market making is not a viable strategy when it comes to relationship markets. So what do you do if you can either be not defined easily in a few parameters, or if there are few others like you in the arranged marriage market? You basically go Over The Counter. Ditch the market and find someone for yourself, or ask people you know to set you up. Or hire a matrimonial advisor who will tell you what to do.

If this doesn’t convince you on why matchmakers are important, then may be you should read what my other half has to say. If she’s the better half or not, you figure.

This is a blogpost that I had planned a very long time (4-5 weeks) ago, and I’m only getting down to write it now. So my apologies if the quality is not as good as my blogposts usually are.

Many of you would have looked at the title of this blogpost and assumed that the trigger for this was the “acquisition” of Joe Rogan’s podcast by Spotify. For a large sum of money, Spotify is “taking his podcast private”, making it exclusive to Spotify subscribers.

However, this is only an “immediate trigger” for writing this post. I’d planned this post way back in April when I’d written one of my Covid-19 related blogposts – maybe it was this one.

I had joked the post needed to be on Medium for it to be taken seriously (a lot of covid related analysis was appearing on Medium around that time). Someone suggested I actually put it on Medium. I copied and pasted it there. Medium promptly took down my post.

I got pissed off and swore to never post on Medium again. I got reminded of the time last year when Youtube randomly pulled down one of my cricket videos when someone (an IP troll, I later learnt) wrongly claimed that I’d used copyrighted sounds in my video (the only sound in that video was my own voice). I had lodged a complaint with Youtube, and my video was resurrected, but it was off air for a month (I think).

Medium and Youtube are both examples of closed platforms. All content posted on these platforms are “native to the platform”. These platforms provide a means of distributing (and sometimes even marketing) the content, and all content posted there essentially belongs to the platform. Yes, you get paid a cut of the ad fee (in case your Youtube channel becomes super powerful, for example), but Youtube decides whether your video deserves to be there at all, and whose homepages to put it on.

The main feature of a closed platform is that any content created on the platform needs to be consumed on the same platform. A video I’ve uploaded on Youtube is only accessible on Youtube. A medium post can only be read on medium. A tweet can only be read on twitter. A Facebook post only on Facebook.

The advantage with closed platforms is that by submitting your content to the platform, you are hoping to leverage some benefits the platform might offer, like additional marketing and distribution, and discovery.

This blog doesn’t work that way. Blogposts work through this technology called “RSS”, and to read what I’m writing here you don’t need to necessarily visit noenthuda.com. You can read it on the feed reader of your choice (Feedly is what I use). Of course there is the danger that one feed reader can have overwhelming marketshare, and the destruction of that feed reader can kill the ecosystem itself (like it happened with Google Reader in 2013). Yet, RSS being an open platform means that this blog still exists, and you can continue to receive it on the RSS reader of your choice. If Medium were to shut down tomorrow, all Medium posts might be lost.

Another example of an open platform is email – it doesn’t matter what email service or app you use, my email and yours is interoperable. India’s Universal Payment Interface (UPI) is another open platform – the sender and receiver can use apps of their choice and still transact.

And yet another open platform (which a lot of people didn’t really realise is an open platform) is podcasting. Podcasts run on the RSS protocol. So when you subscribe to a podcast using Apple Podcasts, it is similar to adding a blog to your Feedly. This thread by Ben Thompson of Stratechery (that I just stumbled upon when I started writing this post) sums it up well:

One thing that has become clear to me over the last week is how few people actually understand how podcasting works.

Lesson number 1: iTunes is not a gatekeeper. It’s a directory, a phonebook if you will, that tells you where to download podcasts.

What Spotify is trying to do (with the Joe Rogan and Ringer deals) is to take these contents off open platforms and put it on its own closed platform. Some people (like Rogan) will take the bait since they’re getting paid for it. However, this comes at the cost of control – like I’m not sure if we’ll have another episode of Rogan’s podcast where host and guest light up a joint.

Following my experiences with Medium and Youtube, when my content was yanked off for no reason (or for flimsy reasons), I’m not sure I like closed platforms any more. Rather, someone needs to pay me a lot of money to take my content to a closed platform (speaking of which, do you know that all my writing for Mint (written in 2013-18) is behind their newly erected paywall now?).

In closing I must mention that platforms being “open” and platforms being “free” are orthogonal. A paid podcast or newsletter is still on an open platform (see Ben Thompson tweetstorm above), since it can be consumed on a medium independent of the one where it was produced – essentially a different feed is generated depending on what the customer has paid for.

Now that I’ve written this post, I don’t know what the point of this is. Maybe it’s just for collecting and crystallising my own thoughts, which is the point behind most of my blogposts anyway.

PS: We have RSS feeds for text and podcasts for audio. I wonder why we don’t have a popular and open protocol for video.

So after a fifteen year gap, I was in the Times of India yesterday, writing about the joys of working from home (I’d shared the clipping yesterday, sharing it again). The interesting thing is that this piece got me the kind of attention that I very rarely got with my six years with the HT Media family (Mint and Hindustan Times).

The main reason, I guess, that this got far more footage, was that it came in a newspaper with a really high circulation. ToI is by far the number one English newspaper in India. While HT may be number two, we don’t even know how much of a number two it is, since it seemingly didn’t participate in the last Indian Readership Survey.

Moreover, ToI is read widely by people in my network. While the same might be true of Mint (at least until its distribution in Bangalore went kaput), it was surely not the case with HT. I didn’t know anyone who read the paper, and since my articles mostly never appeared online, they seemed to go into a black hole.

Another reason why my article got noticed so widely was the positioning in the paper – it was part of ToI’s massively extended “page one” (it came on the back of the front page, which was full of advertisements). So anyone who picked up the paper would have seen this in the first “real page of news” (though this page was filled with analysis of working from home).

On top of all this, I think my mugshot accompanying the article made a lot of difference. While the title of the article itself might have been missed by a few, my photo popping out of there (it helps I have the same photo on my Twitter, Facebook, LinkedIn and WhatsApp – thanks Anuroop) ensured that anyone who paid remote attention to my face would end up reading the article, and that helped me get further reach among my existing network.

ToI is going to pay me a nominal amount for this article, far less than what Mint or HT used to pay me per piece (then again, this one is completely non-technical), but I don’t seem to mind it at all. That it’s given me much more reach among my network means that I’m satisfied with ToI’s nominal payment.

Thinking about it, if we think of newspapers as three-sided markets connecting writers, readers and advertisers, it is possible that others who write for ToI do so for below market prices as well, for it has an incredibly large reach among “people like us”. And that sets the size-related network effects (“flywheel” as silicon valley types like to call it) in action among the writer side as well -you don’t write for money along, and if it can be sort of guaranteed that a larger number of people will read what you write, you will be willing to take lower payment.

In any case, this ToI thingy was a one-off (the last time I’d written for them was way back in 2005, when I was a student – it’s incredible I’ve given this post the same title as that one. I guess I haven’t grown up). But I may not mind doing more of such stuff for them. The more obscure the paper, though, the higher I’ll be inclined to charge! Oh, and henceforth, I’ll insist my mugshot goes with everything I write, even if that lowers my monetary fees.

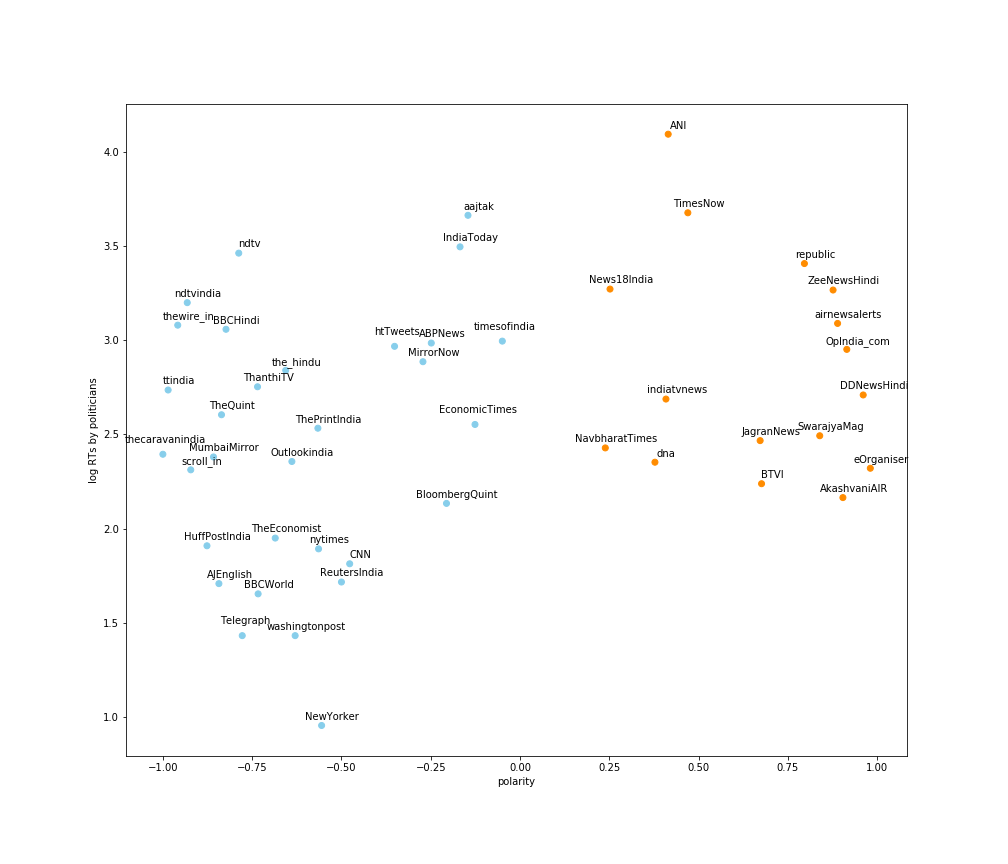

Dibyendu Mishra and Joyojeet Pal of the University of Michigan have some very interesting research out on the political bias of Indian news publications. Rather than do complicated gymnastics such as NLP, they’ve simply looked at the share of articles from each news publication that is retweeted by BJP and non-BJP publications, to draw out a measure of their bias (see link above for methodology).

They have made a nice scatter plot (the other axis is how “popular” these news outlets are in terms of the number of articles retweeted), and looking left to right, you can see the understood (by politicians) bias of various Indian news publications. As Helmet pointed out on Twitter, the most “centrist” news outlets seem to be the Times of India and the Economic Times, both from the Bennett, Coleman and Company group, who people crib about for “being too commercial” and “having too many advertisements”.

Nice idea and analysis.

Moral of story = read TOI and ET for seemingly least biased news! (If you have to read any news at all) https://t.co/EWxiUpnldt

This reminds me of another piece of analysis that was in the news a few months ago, about how subscription-driven online news has led to news outlets being politically polarising. For example, Zach Goldberg did some analysis of frequency of words/phrases in the New York Times that are associated with the extreme left.

1/n Spent some time on LexisNexis over the weekend. Depending on your political orientation, what follows will either disturb or encourage you. But regardless of political orientation, I'm sure we can all say 'holy fucking shit'

The idea is this – when newspapers depended on advertising for most of their funding, they needed to be centrist. Taking political sides meant that large mass-market advertisers wouldn’t want to advertise in this newspaper, and the paper would thus lose revenues. Hence, for the longest time, whatever the quality of the reporting and writing was, news outlets strove to be reasonably politically unbiased – taking sides would mean a loss of money.

Once digital took off, and it became clear that digital advertising wouldn’t really sustain the papers, they started putting their content behind paywalls. And subscription revenues meant two things – news outlets weren’t as beholden to advertisers as they used to be, and it was easier to get paying subscribers if you had a strong ideology. Moreover, online you can provide targeted advertising (rather than mass-market), so you can get away with being biased. And so with the coming of paywalls, newspapers started becoming far more political as the New York Times graph above indicates.

In India, there haven’t been too many publications behind paywalls, but media is evidently getting more and more polarised over time. Papers and channels are branding themselves (implicitly) as being pro or against a particular political party, and that is driving their viewership.

While these media outlets are good for fanbois (and fangirls) of particular ideologies, the ideological bent has meant that it has become harder to get objective news.

And that’s where money, and advertising, comes in.

The positioning of ToI and ET in the middle of the Indian media ideological graph is interesting because they belong to a group that is brazen about commercialisation and revenues (from advertising). And in terms of news objectivity, that’s a good thing. Since ToI and ET are highly money minded, they want to get as much advertising as possible, and in order to attract mass marketers, they need to not be biased.

Taking a political stand means pissing off people belonging to the opposite political persuasion, and that means less readership, which means less advertising revenues. And so if you read the editorials of these newspapers (I read ET everyday), you see that they maintain a careful balance of not appearing too biased in favour or against any party. And you see them raking in the advertisers while more biased (and “ideological”) competitors are forced to request for donations, or put up paywalls restricting their readership.

Putting it another way, there is no surprise that ToI and ET are not biased in their news, and are retweeted by politicians of all persuasions. It is the classic money-driven media model, and that is the one that is capable of providing the most objective news.

I must mention at the outset that this is not a paid post. I haven’t been paid, either in cash or in kind or by any other means, for writing this. This is an honest endorsement, based on principles of market design, on why one of my wife‘s products is awesome.

I spent five minutes this morning interning for my wife. The more perceptive of you will know that she runs Marriage Broker Auntie, a one-stop shop for (right now “arranged”) relationships in India. As part of this, she offers a product called “Market Manager” where she manages people’s matrimonial platform profiles for a fee.

Five minutes of interning as a market management internship convinced me why this is such a great product.

The “job” I did as part of my internship was straightforward. First, I got a lowdown on one of my wife’s clients, and tried to understand him and what he is looking for in a partner. Then, I had to go to shaadi.com (the wife had already opened and logged on on this client’s behalf), where I had to evaluate profiles and decide on whether to send them an “interest” or not (think of this as being similar to swiping left and right on Tinder. Having missed that boat (I met my wife before Tinder had launched), this was interesting).

Every day, Shaadi.com sends each candidate ten “recommended profiles”. My job was to look at these ten on this client’s behalf and decide which of them to pursue. Having achieved the task in five minutes (I might have said yes to two or three of the ten), I was asked what the experience was like.

“I must say I quite enjoyed doing this on behalf of someone else – someone I don’t really know. But doing this for myself or for a close relative would have been nerve-wracking”, I said. And that is precisely why the Market Manager product needs to exist.

Having briefly been in the arranged marriage market before I got lucky enough to met my wife, I know the pains of going through the process. The matrimonial websites have a lot of “market congestion”, in the sense that for every profile you might like, you get shown tens (or even hundreds) of profiles. So sorting through the profiles is a massive task.

Also, the heavy congestion means that both errors of omission and commission can be plenty. It is very possible that you might decide to reject someone who might have been a perfect match for you. It is also possible that you might pursue, and maybe even go on a date with, people who are bad matches for you. And that, as a candidate in the market, can be extremely disheartening.

You send requests to people who you think might make for great spouses for you, but you might end up in their “errors of omission” pile. You lose heart just a little bit each time this happens. Then you look at all the profiles of people who are clearly unsuited to you. And you start wondering if that is your lot. And you lose heart a little bit more.

You lose heart sufficiently that even when an awesome profile comes across, you aren’t sure how to go about it any more. You are jaded. You are unsure of yourelf. Your self esteem has gone to an all-time low. You start wondering what might be wrong with this “awesome profile” that she has expressed an interest in you.

What if someone could instead manage your profile for you, weeding out the clearly unsuitable, and sending on the good matches only once there has been a mutual connect? What if you only got “qualified leads” that you should theoretically have a higher chance of scoring from?

A lot of people employ their parents or close relatives for this purpose, and while the candidates themselves might be saved all the trouble of weeding through and losing heart, you don’t want a parent or close relative to lose heart in your search as well. Moreover, a parent or close relative will only be managing one profile (yours) at a time, and when things don’t go well it’s as easy for them to lose heart as it might be for you.

A professional (such as Marriage Broker Auntie), on the other hand, represents you, understands you and looks out for you, but can also do so in a very dispassionate manner. They manage profiles of several profiles like yours, so the process is something they’ve refined. They know how to handle rejections and congestion without losing heart. And they are great at understanding people and finding out the specific requirements and looking out for them, rather than what a matrimonial site bot can do.

So if you’re right now in the arranged marriage market, do yourself a favour, and employ Marriage Broker Auntieto manage your profile. Yes, the service is not particularly cheap, but in terms of the mental effort saved and increased chances of finding a good match, it will more than easily pay for itself.

Sometimes I wish this service existed 11 years ago, when I was in the market. Then again, I don’t know what would have been the chances of marrying the Marriage Broker Auntie herself if she had been in this business then.

Regular long-time readers of this blog might know that I’m not a big fan of IPO pops (I’ve written about them at least four times so far: one, two, three and four). You can think of this as Number Five, though this is specifically about Direct Listings.

In case you don’t have patience to click through and read my posts, what is the big deal about direct listings? And what is the problem with traditional IPOs? To put it simply, companies looking to raise capital through IPOs are playing a one-time game (you only do an IPO once), while companies that are investing in them are playing a repeated game (they participate in pretty much every IPO that comes on the market – ok may be not WeWork).

This means that investment banks, which stand between the buyer and the seller in such cases, have an incentive to structure the deal to favour the (repeated) buyers, and they price the IPO conservatively. This means that when the company actually lists on the market, it usually does so at a price higher than the IPO price, resulting in a quick win for the IPO investors.

This is injurious for the original investors in the company (founders, VCs, employees) since they are “leaving money on the table”. A pop of 10-20% is considered fair game (a price for the uncertainty on how the market will react to the IPO), but when MakeMyTrip lists 60% higher, or Beyond Meat lists 160% up, it is a significant loss to the early shareholders.

Over the last few months (possibly after the Beyond Meat IPO), Silicon Valley has woken up to this problem of the IPO pop, and suggested that the middleman (equity capital markets divisions of investment banks) be disintermediated from the IPO process. And their vehicle of choice for disintermediation is the direct listing.

A direct listing is what it is. Rather than raising fresh capital from the market, the company picks an auspicious date and declares that on that date its stock will list on the exchanges. The opening auction in the exchange on that day sets what is effectively the IPO price, and the company is public just like that.

Spotify was among the first well-known companies in recent times to do a direct listing, when it went public in 2018. Earlier this year, Slack did a direct listing as well. Here is Benchmark Capital’s Bill Gurley (a venture capitalist) on the benefits of a direct listing.

Direct Listing is all well and good when a company doesn’t have to raise capital. The question is how do you go public while at the same time raising capital (which is what a traditional IPO does)? Slack and Spotify were able to do the direct listing because they didn’t want capital from the IPOs – they just wanted to offer liquidity to their investors.

The New York Stock Exchange thinks it can be done, and has proposed a product where companies can use the opening daily auction to price the new shares being offered. There are issues, of course, about things like supply of shares, lock-ups, price support and so on, but the NYSE thinks this can be done.

NYSE’s President Stacey Cunningham recently appeared on the a16z podcast (again run by a VC, notice!) and spoke eloquently about the benefits of direct listing.

The SEC (stock regulator in the US) isn’t very happy with the proposal, and rejected it. Traditional bankers are not happy with the NYSE’s proposal, either, and continue to find problems with it (my main source of this angst is Matt Levine, who is a former ECM Banker and who thus has solid reasons as to why ECM Bankers should exist). In any case, the NYSE has refiled its proposal.

So what is the deal with direct listings?

In a way, you can think about them as a way to simply disintermediate the market. The ECM Banker, after all, is a middleman who stands between the buyer (IPO investor) and seller (company raising capital), helping them come up with a smooth deal, for a fee. The process has been set for about 40 years now, and has become so stable that the sellers think it has become unfair to them. And so there is the backlash.

Until now, the sellers were all independent entities with their own set of investors, and so they were unable to coordinate and express their displeasure with the IPO process. The buyers, on the other hand, play the game repeatedly, and can thus coordinate among themselves and with the middlemen to give themselves a sweet deal.

The development in this decade is that the same set of VC investors invest in a large number of go-to-public companies, and so suddenly you have sellers who are present across deals, and that has changed the game in a sense. And so direct listings are on every tech or investing podcast.

Among the things I wrote in my book (which came out a bit over two years ago) is that one important role that middlemen play is to reduce uncertainty and volatility in the market.

One concern with direct listings is that there can be a wide variation in the valuations by different players in the market, and the opening auction is not an efficient enough process to resolves all these variations. The thing with the Spotify and Slack listings was that there was a broad consensus on the valuation of these companies (more in line with public company valuations), a set of investors who wanted to get in and a set of investors who wanted to get out. And so it all went smoothly.

But what do you do with something like WeWork? The problem with private market valuations is that with players like SoftBank, they can be well divorced from market realities. In WeWork’s case, the range of IPO valuations that came up differed by an order of magnitude. And that kind of difference is not usually reconcilable in one normal opening auction (imagine a bid of 8 billion and an ask of 69 billion, and other numbers somewhere in between) without massive volatility going forward. In that sense, the attempted traditional IPO did a good job of understanding demand and supply and just declaring “no deal”. “No deal” is usually not an option when you do a direct listing.

OK I’ve written a lot I know (this is already 2X the length of my usual blog posts), so what do I really think about IPOs? I think all this talk about direct listings will shift the market ever so slightly in favour of the sellers. Companies will follow a mixed strategy – well known companies (consumer brands, mostly) with stable valuations will go for direct listings. Less well known companies, or those with unstable valuations will go for IPOs.

And in the latter case, I predict that we will move closer to a Dutch auction (like what Google did) among the investors rather than the manual allocation process that ECM bankers indulge in nowadays. It will have the benefit of large blocks being traded at time zero, at a price considered fair by everyone, and hopefully low volatility.

The Ken, where I bought a year long subscription today, has a brilliant piece on the ad agency business (paywalled) in India. More specifically, the piece is on pricing in the industry and how it is moving from a commissions only basis to a more mixed model.

Advertising agencies perform a dual role for their clients. Apart from advising them on advertising strategy and helping them create the campaigns, they are also in charge of execution and buying the advertising slots – either in print or television or hoardings (we’ll leave online out since the structure there is more complicated).

As far as the latter business (acquisition of slots to place the ad – commonly known as “buying”) is concerned, typically agencies have operated on a commission basis. The fees charged has been to the extent of about 2.5% of the value of the inventory bought.

In financial markets parlance, advertising agencies have traditionally operated as brokers, buying inventory on behalf of their clients and then charging a fee for it. The thrust of Ashish Mishra’s piece in ate Ken is that agencies are moving away from this model – and instead becoming what is known in financial markets as “dealers”.

Dealers, also known as market makers, make their money by taking the other side of the trade from the client. So if a client wants to buy IBM stock, the dealer is always available to sell it to her.

The dealer makes money by buying low and selling high – buying from people who want to sell and selling to people who want to buy. Their income is in the spread, and it is risky business, since they bear the risk of not being able to offload inventory they have had to buy. They hedge this risk by pricing – the harder they think it is to offload inventory, the wider they set the spreads.

Similarly, going by the Ken story, what ad agencies are nowadays doing is to buy inventory from media companies, and then selling it on to the clients, and making money on the spread. And clients aren’t taking too well to this new situation, subjecting the dealers ad agencies to audits.

From a market design perspective, there is nothing wrong in what the ad agencies are doing. The problem is due to their transition from brokers to dealers, and their clients not coming to terms with the fact that dealers don’t normally have a fiduciary responsibility towards their clients (unlike brokers who represent their clients). There are also local monopoly issues.

The main service that a dealer performs is to take the other side of the trade. The usual mechanism is that the dealer quotes the prices (both buy and sell) and then the client has the option to trade. If the client feels the dealer is ripping her off, she has a chance to not do the deal.

And in this kind of a situation, the price at which the dealer obtained the inventory is moot – all that matters to the deal is the price that the dealer is willing to sell to the client at, and the price that competing dealers might be charging.

So when clients of ad agencies demand that they get the inventory at the same price at which the agencies got it from the media, they are effectively asking for “retail goods at wholesale rates” and refusing to respect the risk that the dealers might have taken in acquiring the inventories (remember the ad agencies run the risk of inventories going unsold if they price them too high).

The reason for the little turmoil in the ad agency industry is that it is an industry in transition – where the agencies are moving from being brokers to being dealers, and clients are in the process of coming to terms with it.

And from one quote in the article (paywalled, again), it seems like the industry might as well move completely to a dealer model from the current broker model.

Clients who are aware are now questioning the point of paying a commission to an agency. “The client’s rationale is that is that it is my money that is being spent. And on that you are already making money as rebate, discount, incentive and reselling inventory to me at a margin, so why do I need to pay you any agency commissions? Some clients have lost trust in their agencies owing to lack of transparency,” says Sodhani.

Finally, there is the issue of monopoly. Dealers work best when there is competition – the clients need to have an option to walk away from the dealers’ exorbitant prices. And this is a bit problematic in the advertising world since agencies act as their clients’ brokers elsewhere in the chain – planning, creating ads, etc.

However the financial industry has dealt with this problem where most large banks function as both brokers and dealers. It’s only a matter of time before the advertising world goes down that path as well.

The market for homosexual relationships is an interesting one from the analysis perspective. Like the market for heterosexual relationships, it is a matching market (we are in a relationship if and only if I like you AND you like me). Unlike heterosexual relationships, it is not a “bipartite” market, since both the nominal “buyer” and the “seller” in a transaction will come out (no pun intended) of the same pool (gay people of a particular sex).

The other factor that makes this market interesting (purely from an analysis perspective – it’s bad for the participants) is that there is disapproval at various levels for homosexual relationships. Until today, for example, it was downright criminal to indulge in gay sex in India. Even where it is legal, there is massive social and religious opposition to such relationships (think of the shootout at the gay bar in Florida, for example).

Social disapproval has meant that gays sometimes try to keep their sexuality under wraps. Historically, it has been a common practice for gays to enter into heterosexual marriages, and pursue relationships outside. In fact, there is nothing historical about this – read this excellent piece by Srinath Perur on gays in contemporary hinterland Karnataka, for whom Mohanaswamy, a collection of short stories with a gay protagonist, was a kind of life changer.

Organising a market for an item that is illegal, or otherwise frowned upon, is difficult, since people don’t want to be found participating in it. If I were a gay man looking for a partner, for example, I couldn’t go around openly looking for one if I didn’t want my family to know that I’m gay. So the first task would have been discovery – “safe spaces” where I would be happy to expose my sexuality, and where I could also meet potential partners.

When demand and supply exist, buyers and sellers will find a way to meet each other, though often at high cost. One such “way” for homosexual people has been the gay bar. Though not explicitly advertised, such bars act as focal points (I have a chapter on focal points in my book) for gay people.

They also act as an “anti focal point” (a topic I HAVEN’T covered in the book, for a change!) for heterosexual people who want to stay away because they don’t want to be hit on by gay people (thus reducing market congestion – another topic I cover in my book). Similarly other cultural activities have acted as focal points for gay people to get together and meet each other.

Like in heterosexual relationship markets (this is the link to a sample chapter from the book), the advent of dating apps has revolutionised gay dating, as apps such as Tinder and Grindr have provided safe spaces where gays can look for relationships “from the comfort of their homes”. There are studies that show that Grindr has changed the nature of relationships among gay men, and how these apps have “saved lives” in places such as India where homosexuality was criminal until today.

Today’s Indian Supreme Court ruling will have a massive positive impact on gay relationships in India. For starters, there are still millions of people in the closet – while apps such as Tinder and Grindr allowed more people to participate in these markets (since this could be done without really “coming out”), that gay sex was a criminal act would have led to some people to err on the side of caution (and deprive themselves of the chance of a relationship). Gay people who were worried about criminality, but not that much about social sanctions, will now be more willing to come out, leading to an increase in the market size.

Barring congestion (when “bad counterparties” prevent you from finding “good counterparties”), the likelihood of finding a match in a market is generally proportional to the number of possible counterparties. Since gay relationship markets are not bipartite, we can say that the likelihood of finding a good match varies by the square of the number of market participants (and this brings in the Indian Prime Minister’s infamous 2ab term). In other words, it not only allows the people now coming into the market to find relationships, but it also allows existing players to find better relationships.

Then, there is the second order effect. Decriminalisation will mean that more people will come out of the closet, which will mean more people will find homosexuality to be “normal” leading to better social mores (to take a personal example, I used to use the word “gay” as a pejorative (to mean “uncool”) until I encountered my first openly gay acquaintance – someone with whom I share on online mailing list). And as social attitudes towards homosexuality change, it will lead to more people coming out of the closet, setting off a virtuous cycle of acceptance of homosexuality.

In other words, today’s decision by the Indian Supreme Court is likely to set off a massive virtuous cycle in the liquidity of the market for homosexual relationships in India!

PS: It is a year since my first book was published, so we are running a promotional offer where you can buy the Kindle version for one dollar (or Rs. 70).